KISS Software / Blog / blockchain / What Is Blockchain: Yevhen Kasyanenko Explains Blockchain In Simple Terms

#blockchain

What Is Blockchain: Yevhen Kasyanenko Explains Blockchain In Simple Terms

4.9

11

What Is Blockchain: Yevhen Kasyanenko Explains Blockchain In Simple Terms

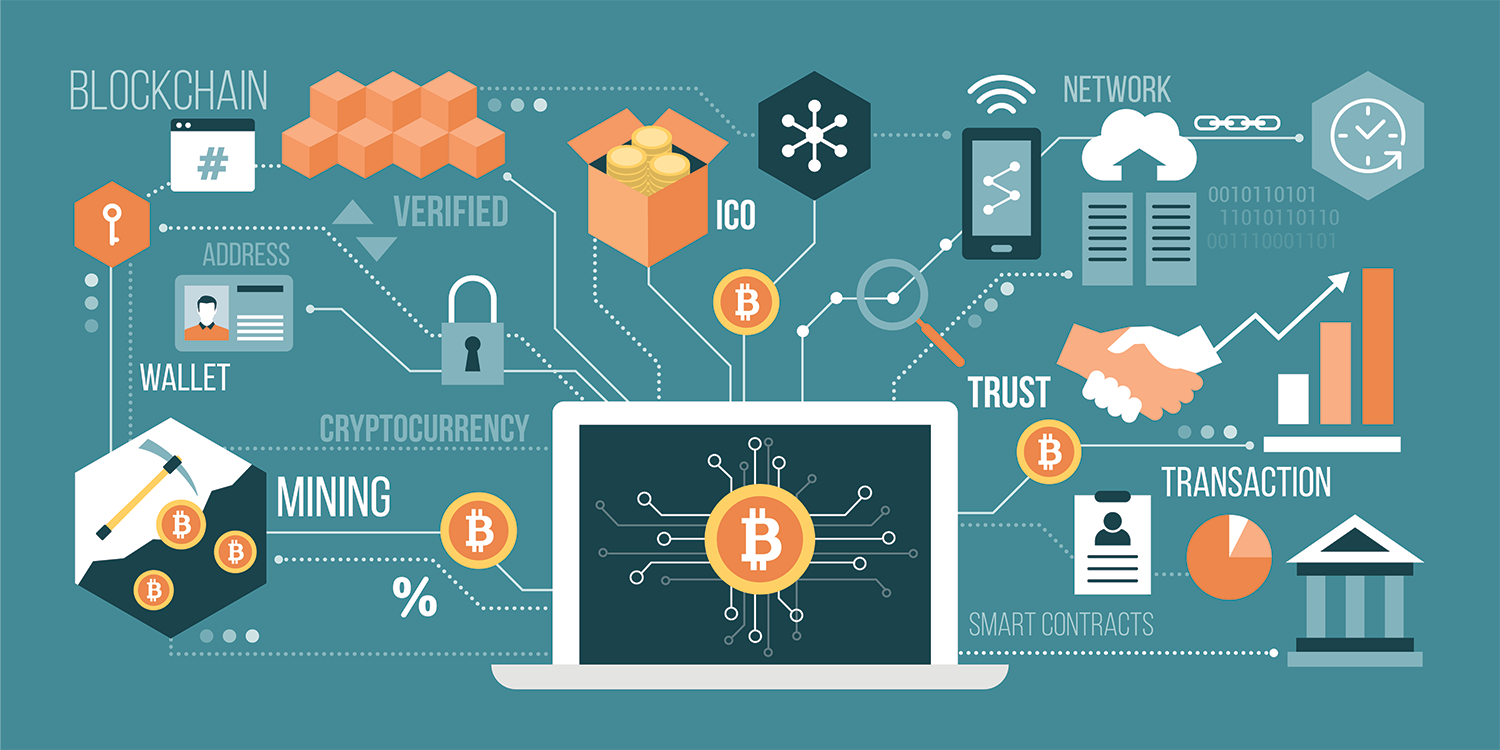

And hello again! This is Yevhen Kasyanenko, and today we continue exploring how modern technologies can enhance your business. In today’s blog on Kiss.software, I’ll be telling you about blockchain. Get comfortable, and let’s dive in. Ok Google, what is blockchain? Blockchain is a decentralized digital system. Its main purpose is to store and transfer data. The entire system is built from blocks linked together by cryptographic algorithms.

Each block in the chain contains information about transactions and the hash of the previous block. Why is this necessary? The system guarantees immutability, transparency, and data security.

And most importantly, the system itself lacks a central governing authority. All information and data are distributed among users. Such a system is significantly safer and more reliable than traditional data protection mechanisms.

That is why blockchain development is becoming a key tool for creating reliable, decentralized, and secure systems capable of providing a high level of trust and efficiency in any field of activity.

Do you need blockchain technology integration for your project? The K.I.S.S. Software team is ready to help. The team consists of specialists in blockchain solutions for businesses.

Invest in the future of your business today! Order a turnkey blockchain solution from the professionals at K.I.S.S. Software and gain a competitive advantage.

Order an innovative blockchain solution for your business right now!

We, the K.I.S.S. Software team, are ready to develop and implement a custom blockchain solution for you that will make your business more secure, transparent, and efficient. Fill out the application, and we’ll start creating the future of your project today!

Well, let’s dive deeper into how the system works. First, I’ll explain the complex part in a complex way, and then I’ll simplify it. Ready? Here’s a step-by-step guide on how blockchain works:

Step 1. Creating a transaction

Let’s say we have a trader named Alex. He really wants to transfer 10 BTC to his friend Bob (yes, they’re not short on funds). Alex logs into an exchange or his crypto wallet and creates a transaction.

To proceed with the transaction, he specifies the amount of coins and the recipient’s address.

A transaction on the network is a record that contains the following information:

Sender’s address.

Recipient’s address.

Transfer amount (10 BTC).

Sender’s signature. This is a unique digital signature that confirms the transaction was indeed created by Alex and not by a fraudster.

Step 2. Verification.

Once the transaction is created, it is sent to the blockchain network. There, it undergoes verification by network participants called nodes. These nodes check the following:

Sender’s signature. It must be confirmed that the signature belongs to Alex and that he has the right to manage these funds.

Sender’s balance. It is verified that Alex indeed has 10 BTC to transfer to Bob.

Step 3. Block formation.

The transaction has been verified. What’s next? Next, transactions are grouped together to form a new block. The block contains the following information:

Transaction list. Includes Alex and Bob’s transaction, as well as others awaiting confirmation.

Hash of the previous block. This is a unique identifier that links the new block to the previous one.

Timestamp. Displays the exact time the block was created.

Step 4. The block is added to the chain.

To add a new block to the chain, nodes must reach a consensus. This is achieved using a consensus algorithm:

Proof of Work (PoW). Nodes or miners compete to solve a specific mathematical problem. The one who solves it faster than others gets to add the block to the chain. For this, they receive a reward in cryptocurrency.

Proof of Stake (PoS). Participants stake their assets as collateral. The mechanism is straightforward: the larger the share in the overall pool, the higher the probability that your block will be added to the chain.

Step 5. Ledger update.

The new block has been added to the chain. The entire network is updated. Every participant in the network receives a copy of the updated blockchain, now including the new block. That’s it, the entire network now knows about Alex and Bob’s transaction.

Step 6. Final.

The block is now added to the chain. The transaction between Alex and Bob is complete. Bob receives 10 BTC, and this information is permanently recorded in the blockchain.

Simply About the Complex: How Does Blockchain Work?

Still curious but not quite clear? Let me explain in simpler terms. Think of blockchain as a digital chain of records.

Here’s an easy analogy: imagine blockchain technology as a giant book that every market participant has. Every user can make their own entries in this book (each transaction or action creates a record and forms its own data block).

Other users can see these entries but cannot alter the data in any way. Blockchain technology does not allow records to be changed, rearranged, or erased.

Each block of data (an entry in the book) is linked to previous blocks (entries). If someone tries to disrupt the integrity of the chain, others will immediately notice.

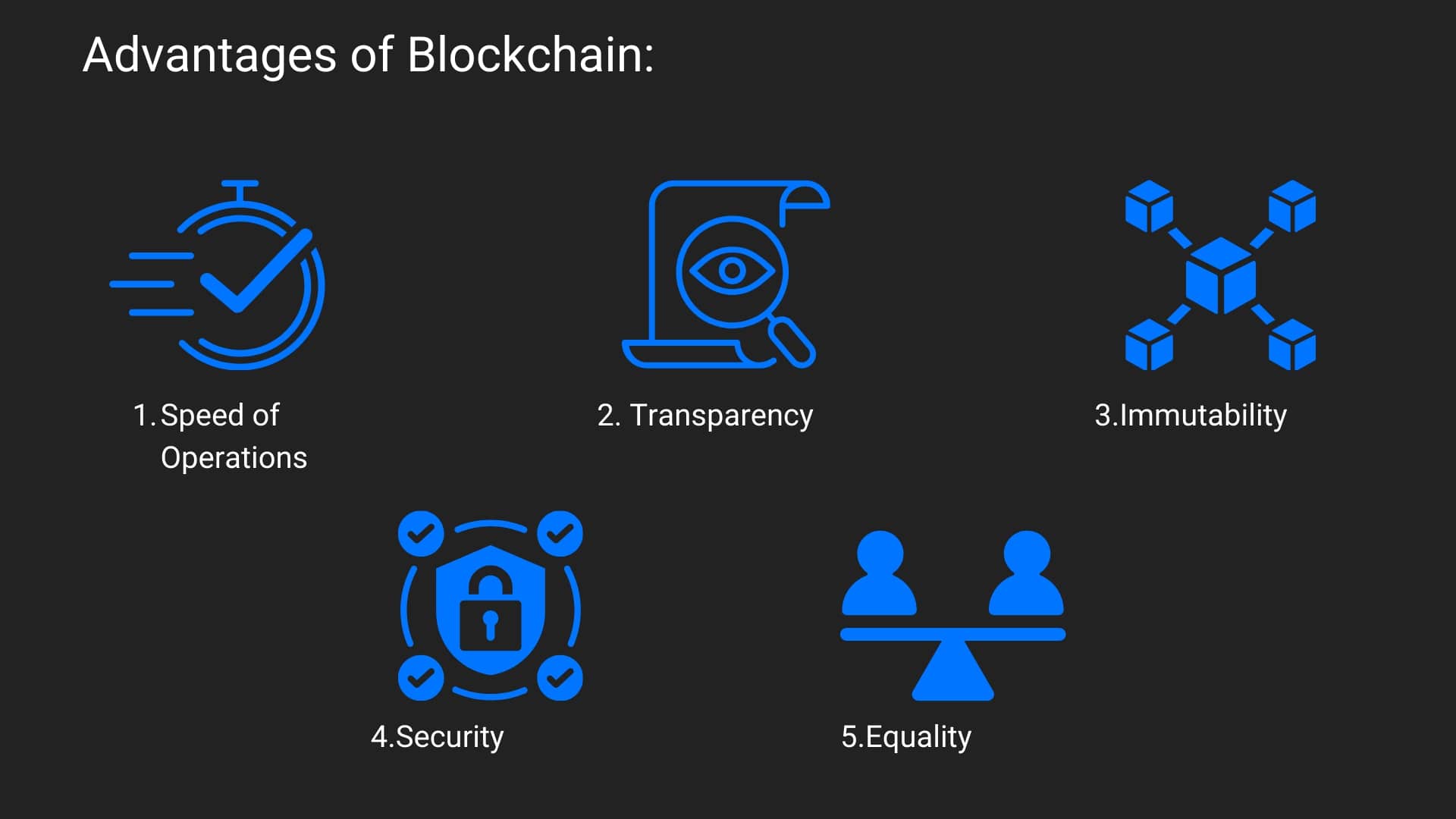

Advantages of Blockchain

And now it’s time to delve into the advantages of blockchain technology. It’s clear that they exist, given its popularity.

We’ve already established that blockchain technology operates without a central governing body. All information is distributed among participants. With this system’s algorithm, manipulations “from above” are simply impossible because there is no governing body.

All user actions (authorizations, transfers, purchases, sales, signatures) are automatically recorded and appear in the shared ledger. And yes, every other participant in the system can view them.

Data that is already in the chain cannot be deleted. It’s simply impossible. This feature makes the technology an ideal option for working with data.

The security of the entire system is built on unique data encryption methods called cryptographic. Thanks to this method of data encryption, blockchain has become one of the most reliable systems in the world.

Tired of intermediaries and countless third parties? Blockchain will help you, as it completely eliminates the need for intermediaries, whether in Uzbekistan or the USA. No banks, no notaries, no unnecessary entities. Just you and your partner.

Automatic fulfillment of contract terms has become possible thanks to smart contracts. They are what make the system so fast.

Blockchain is versatile. You could even say that its applications are limited only by your imagination and your development team.

Transparency and security of the system

Let’s be honest: when the technology first became publicly available, no one believed in it. The main argument against it was, “No leadership, no company, no headquarters, and all users know everything about everyone!” But the reality turned out to be completely different.

The transparency of the entire system and its processes became its key advantage. In traditional systems, data and information are hidden from the average user, while in blockchain, it’s the opposite.

All network participants can see transactions and information about them.

Each block in the chain contains a cryptographic hash. This hash is created based on the block itself. The hash protects the block from unauthorized changes.

How does a new block appear in the chain? The mechanism might seem complicated, but here’s how it works: all participants must reach consensus or agreement. Two algorithms, Proof of Work and Proof of Stake, are used to achieve this consensus. These algorithms are responsible for adding new blocks.

In traditional data systems, information is stored on a centralized server. In contrast, blockchain distributes data among all participants. Even if some links attempt to hack or modify the data, the overall network remains secure.

Saving Resources and Increasing Business Efficiency

Let’s not forget two factors that play a key role in business and projects: system efficiency and cost savings.

Traditional bank transfers are not always convenient. Due to fees and additional checks, funds can take days, or even weeks, to reach the recipient.

Blockchain overcomes this limitation. Transfers take no more than a few minutes.

Process automation allows you to reduce costs on documentation, legal services, and administration. The technology is actively used in real estate, enabling fast and simple property registration.

The immutability of data in the chain has its benefits. Users can always trust the accuracy of the information, significantly reducing the need for audits and additional data checks.

Integrating blockchain technologies improves company security, transparency, and helps save resources. Thanks to these advantages, blockchain integration is gaining popularity. While blockchain development may initially cost more, in the long run, the project’s expenses will be significantly lower.

Examples of Blockchain Use

As they say, from theory to practice? Let’s take a closer look at who, where, and how blockchain technologies can be used.

Financial Sector

I’ve already mentioned transaction speed, but it’s worth reiterating. Speed is crucial for modern business, and that’s where blockchain comes in.

Its integration can simplify the payment for goods and services and enhance financial management systems. But that’s not all.

As I noted earlier, international bank transfers are slow and costly. Why not integrate blockchain to expedite the process and eliminate intermediaries? Yes, there are fees when transferring crypto (which depend on the coin and the network, but that’s another story). The difference in transfer fees is evident: $0.50 or $500 (if using banking services).

Automate the execution of agreements between parties. Thanks to smart contracts, you can stop tolerating unnecessary intermediaries. Automate the systems for lending, insurance, and asset management.

Logistics and Supply Chains

In this niche, another important advantage of blockchain is operational transparency. You can track the entire supply chain of goods, allowing you to manage risks and maintain high-quality standards.

In the food industry, blockchain is used to monitor product quality, storage conditions, and delivery.

Additionally, blockchain technologies aid in managing supplier relationships. How? You can monitor and analyze supplier performance, creating records of interactions with the product at various stages of the logistics chain.

Real Estate and Land Market

In the real estate sector, blockchain has been actively used for some time now.

Blockchain allows assets to be divided into digital tokens, enabling fractional ownership of property. This means that without commissions and intermediaries, an investor can easily acquire a share in real estate (be it commercial property, residential buildings, or even land).

Smart contracts in real estate allow for the automation and acceleration of transactions. Imagine being able to buy property in just 2 minutes. Yes, literally in 2 minutes, as ownership rights will be transferred automatically.

You can create a unified, secure, and fully transparent registry of property rights for land parcels.

Why Us?

Well, I’ve covered the basics of blockchain technology. To discuss all its potential applications, we could easily write several more long reads.

Blockchain is a functional and even revolutionary tool for business. Ignoring its capabilities means relinquishing your place in the global market.

If I’ve piqued your interest, it’s time to reach out to professionals.

The K.I.S.S. Software team consists of experts with many years of experience in digital solutions for businesses.

For each task, we form a dedicated team of specialists from various fields.

We guarantee an individual approach to every project.

We don’t just create turnkey digital products; we provide long-term support and updates.

We will always be in touch so that you can assess results and make timely adjustments.

Working with K.I.S.S. Software ensures that your project will be implemented with consideration of all the requirements and nuances of your business. We help integrate blockchain into your business to fully unlock its potential.

The process of blockchain technology development

1

Step 1.

2

Step 2.

3

Step 3.

4

Step 4.

5

Step 5.

6

Step 6.

1

Step 1.

2

Step 2.

3

Step 3.

4

Step 4.

5

Step 5.

6

Step 6.

Step 1. Goal setting

This step analyses the challenges that blockchain will address, such as decentralising data or automating processes. The type of network is selected: public for open access, private for internal use, or consortium for groups of organisations.

Time to deliver

~ 1-2 weeks

Step 2. Platform selection

A suitable blockchain platform is identified, such as Ethereum for smart contracts or Hyperledger for enterprise solutions. Factors such as scalability, performance and transaction costs are considered.

Time to deliver

~ 2-3 weeks

Step 3. Architectural design

Block structure, consensus algorithm (e.g. Proof of Stake) and access control mechanisms are developed. The design includes the creation of smart contracts and customisation of network node interactions.

Time to deliver

~ 3-4 weeks

Step 4. Development and testing

Smart contracts, interfaces and network components are created and then tested on test platforms. Functionality, performance and vulnerability protection are tested.

Time to deliver

~ 2-3 weeks

Step 5. Network deployment

The blockchain is launched on the core network with nodes and infrastructure set up. Integration with other systems and deployment of smart contracts is carried out.

Time to deliver

~ 2-3 weeks

Step 6. Support

Ensures stable network operation through monitoring, updating and error correction. New features are also implemented to improve efficiency and scalability.

Time to deliver

~ 1-2 weeks

Order an innovative blockchain solution for your business now!

We, the K.I.S.S. Software team, are ready to develop and implement for you a customised blockchain solution that will make your business more secure, transparent and efficient. Fill out an application form and we will start creating the future of your project today!